RNNとは

リカレントニューラルネットワーク

時系列データを扱う「時間」という概念を取り入れたニューラルネットワーク

LSTMやGRUという手法がある。

降水量、株価、為替などが時系列データにあたる。

LSTM

Long-Short-Term-Memoryの略

長期・短期の時間依存性を保つ。

RNNの実践

Udemyの講座のDeep Learning A-Z™: Hands-On Artificial Neural Networksを参考にしています。

プログラム

上で紹介されているプログラムを少し書き換えて、処理を軽くしています。

具体的には、

- LSTMの層を減らしました

- エポック数を偉しました

- 全結合層を1層足しました

この3点を変更しました。

ソースコード

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

# 訓練データ

dataset_train = pd.read_csv('Google_Stock_Price_Train.csv')

training_set = dataset_train.iloc[:, 1:2].values

# Feature Scaling

from sklearn.preprocessing import MinMaxScaler

sc = MinMaxScaler(feature_range = (0, 1))

training_set_scaled = sc.fit_transform(training_set)

# Creating a data structure with 60 timesteps and 1 output

X_train = []

y_train = []

for i in range(60, 1258):

X_train.append(training_set_scaled[i-60:i, 0])

y_train.append(training_set_scaled[i, 0])

X_train, y_train = np.array(X_train), np.array(y_train)

# Reshaping

X_train = np.reshape(X_train, (X_train.shape[0], X_train.shape[1], 1))

#RNNの構築

# Keras

from keras.models import Sequential

from keras.layers import Dense

from keras.layers import LSTM

from keras.layers import Dropout

# Initialising the RNN

regressor = Sequential()

# Adding the first LSTM layer and some Dropout regularisation

regressor.add(LSTM(units = 50, return_sequences = True, input_shape = (X_train.shape[1], 1)))

regressor.add(Dropout(0.2))

regressor.add(LSTM(units = 50))

regressor.add(Dropout(0.2))

# Adding the output layer

regressor.add(Dense(units = 20))

regressor.add(Dense(units=1))

# Compiling the RNN

regressor.compile(optimizer = 'adam', loss = 'mean_squared_error')

# Fitting the RNN to the Training set

regressor.fit(X_train, y_train, epochs = 20, batch_size = 32)

# Part 3 - Making the predictions and visualising the results

# Getting the real stock price of 2017

dataset_test = pd.read_csv('Google_Stock_Price_Test.csv')

real_stock_price = dataset_test.iloc[:, 1:2].values

# Getting the predicted stock price of 2017

dataset_total = pd.concat((dataset_train['Open'], dataset_test['Open']), axis = 0)

inputs = dataset_total[len(dataset_total) - len(dataset_test) - 60:].values

inputs = inputs.reshape(-1,1)

inputs = sc.transform(inputs)

X_test = []

for i in range(60, 80):

X_test.append(inputs[i-60:i, 0])

X_test = np.array(X_test)

X_test = np.reshape(X_test, (X_test.shape[0], X_test.shape[1], 1))

predicted_stock_price = regressor.predict(X_test)

predicted_stock_price = sc.inverse_transform(predicted_stock_price)

# Visualising the results

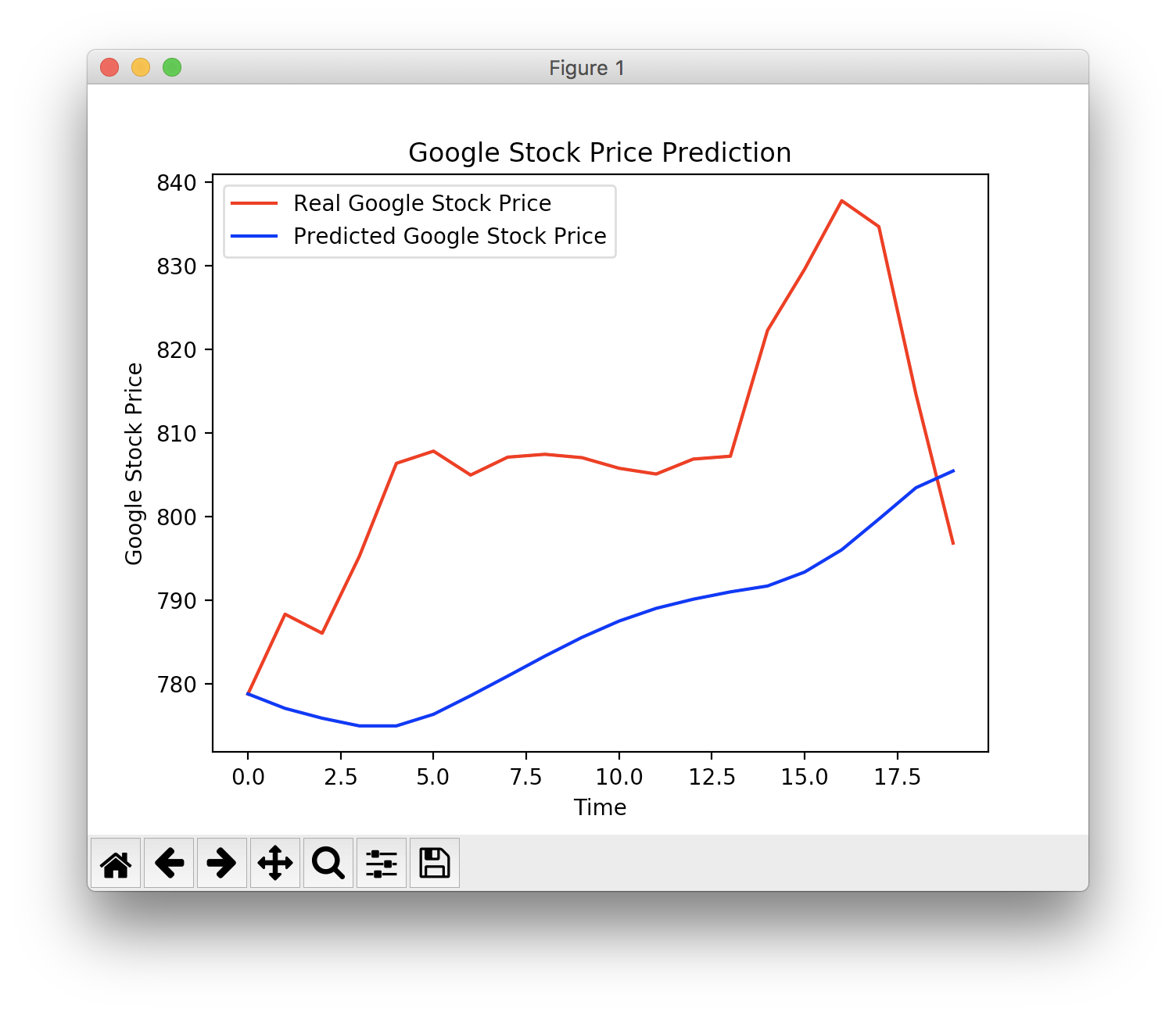

plt.plot(real_stock_price, color = 'red', label = 'Real Google Stock Price')

plt.plot(predicted_stock_price, color = 'blue', label = 'Predicted Google Stock Price')

plt.title('Google Stock Price Prediction')

plt.xlabel('Time')

plt.ylabel('Google Stock Price')

plt.legend()

plt.show()

結果